Time-Series Analysis

Important Concepts, Handy Techniques, and Some Cautionary Tales

A travel tip…or Zoli as an unintentional travel agent?

This presentation

40 minutes

Superweek

5 days

My last job

5 years

Yehoshua’s intros

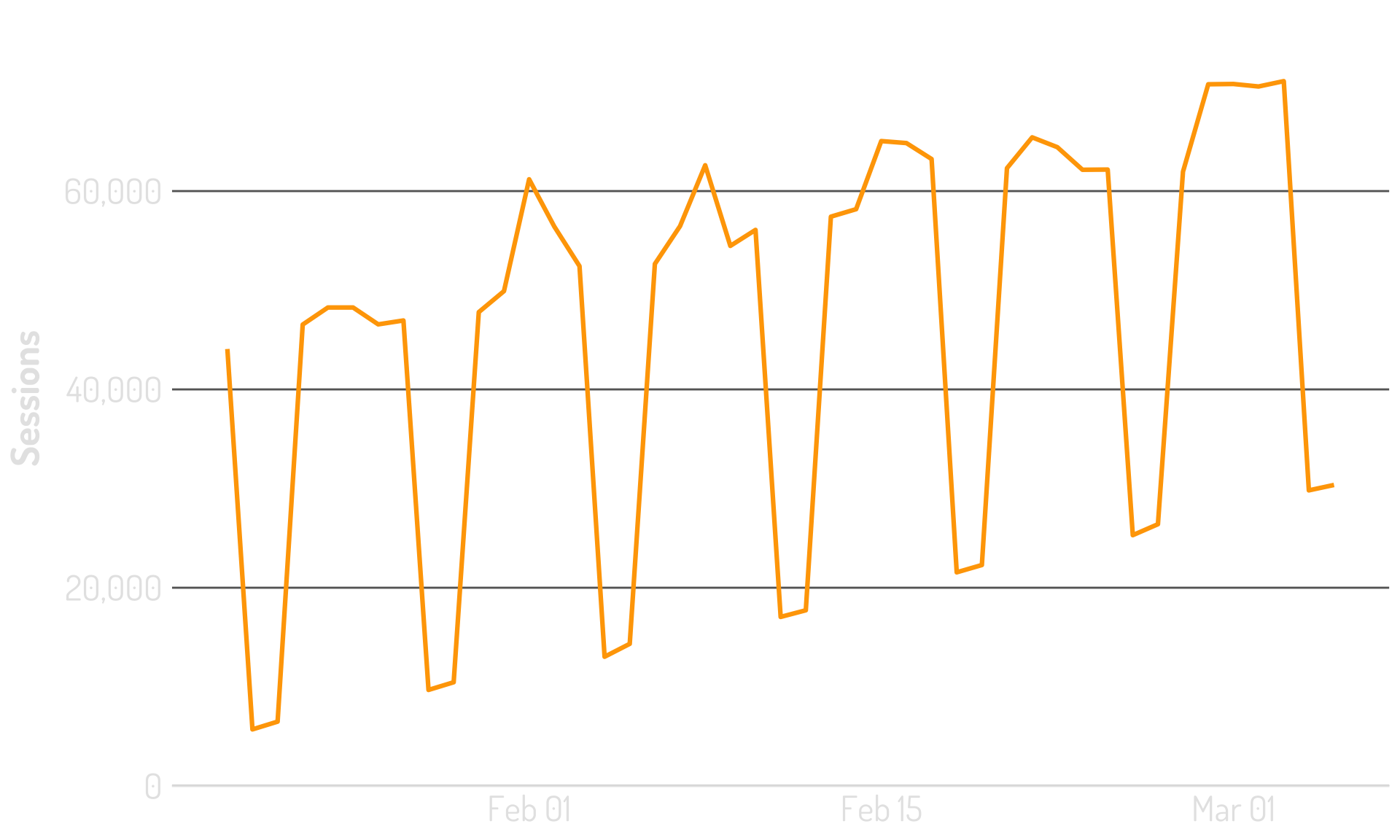

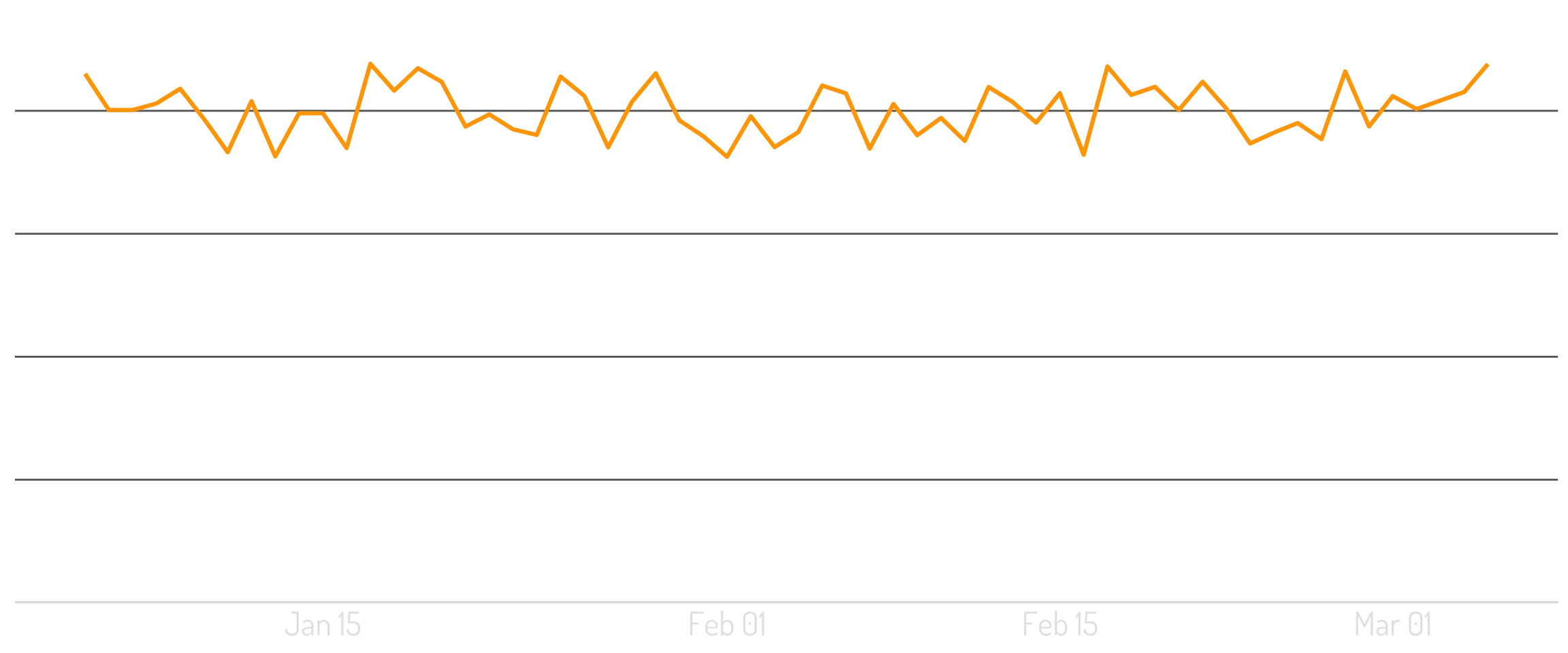

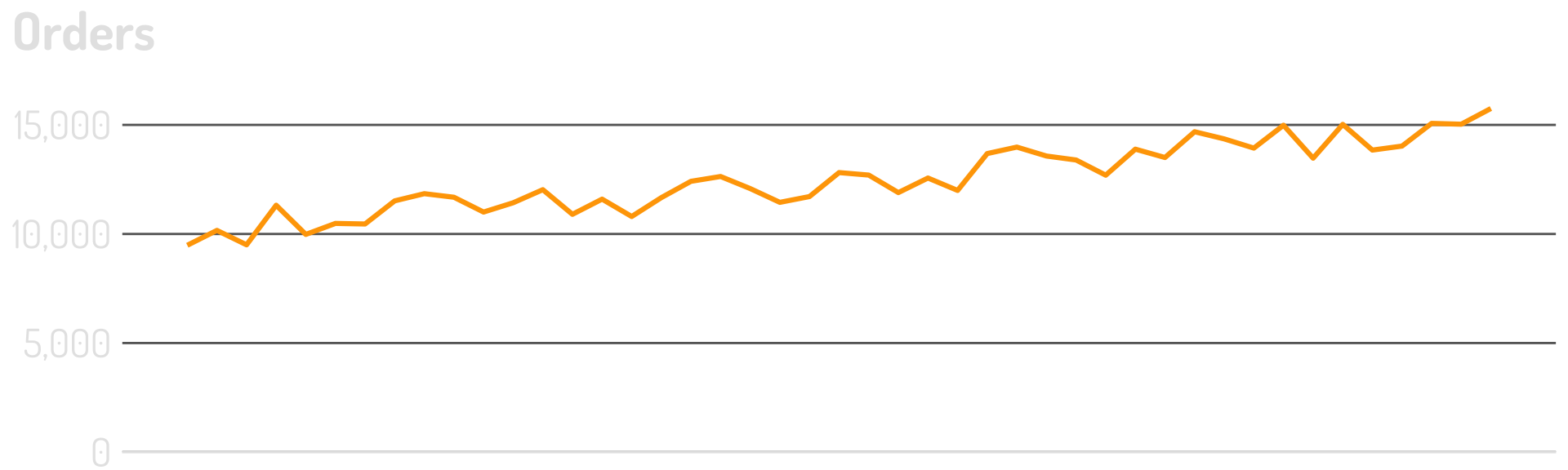

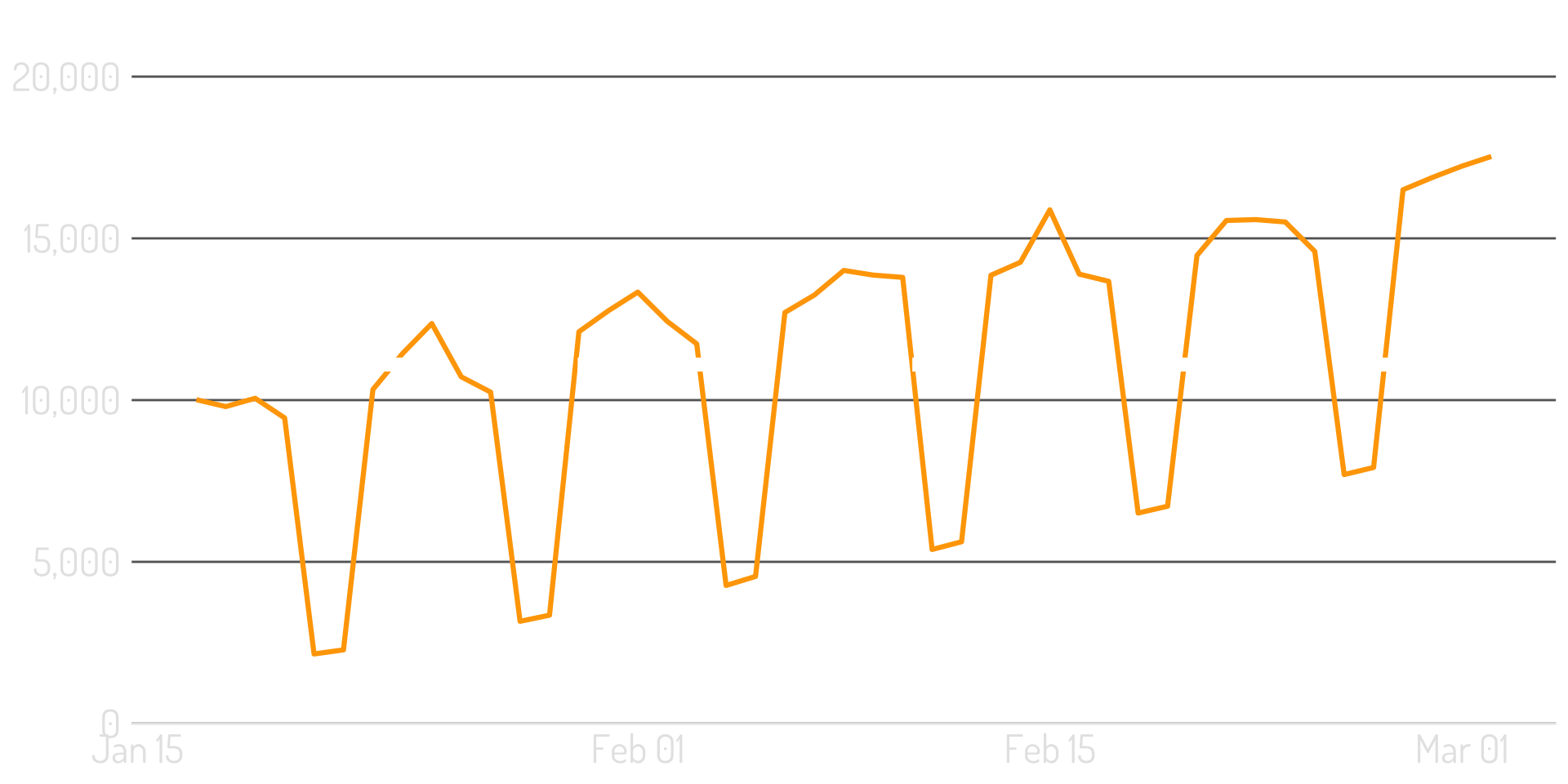

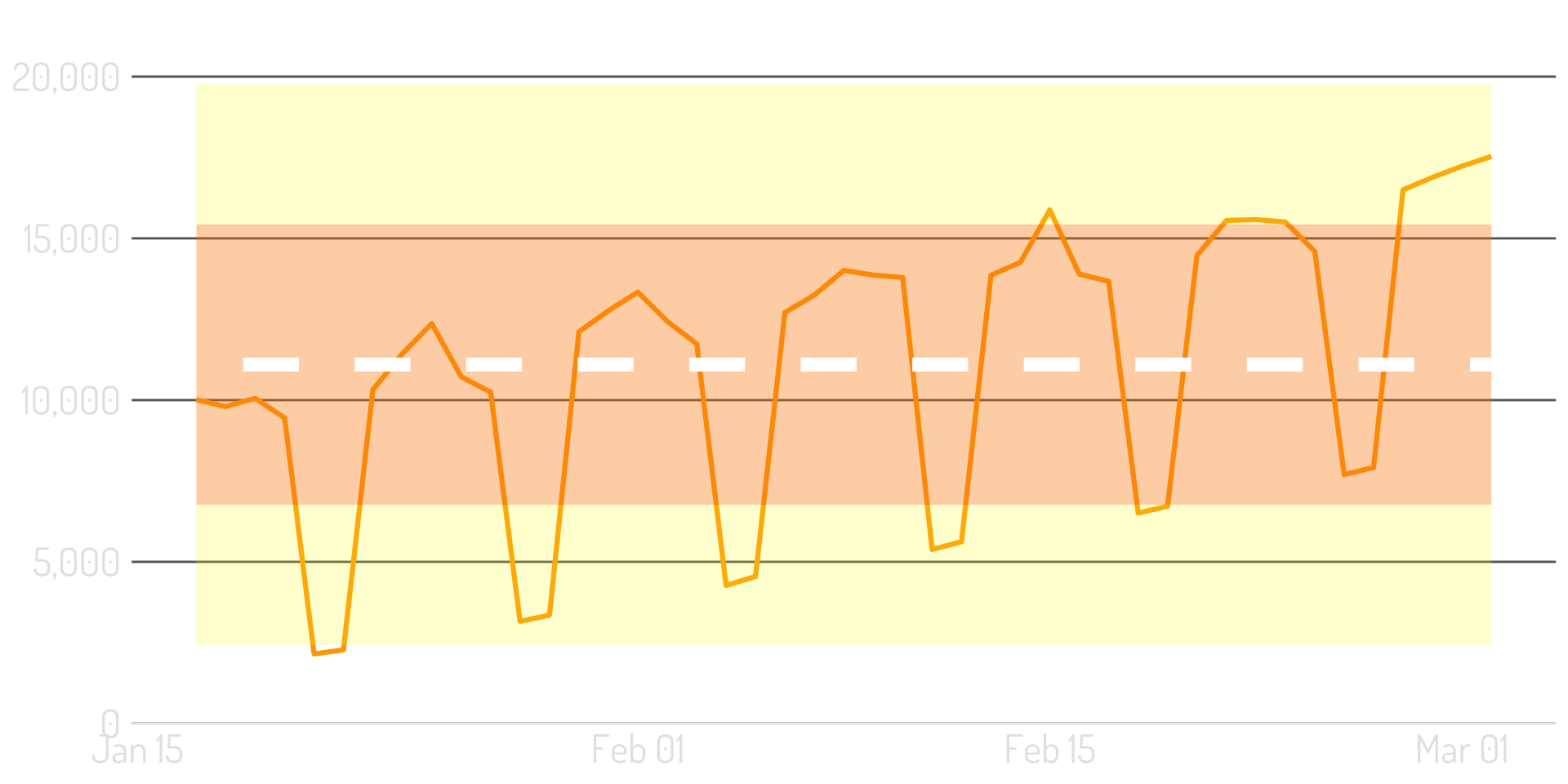

It rarely looks quite like this

It often has a weekly cycle to it

And it may have a trend to it

Let’s think about statistics

Our data exists over time.

So, what is our population?

Is it the past to the present?

Maybe. Maybe not.

Maybe it’s the past, present, and future?

Or…just the future?

But…we can’t sample from the future!

So…what is our sample?

Our sample is a sample timeframe.

This is imperfect.

Because our reality is constant change.

A stationary time series is one whose statistical properties do not depend on the time at which the series is observed. 1

A stationary time series is one whose statistical properties do not depend on the time at which the series is observed. 1

A stationary time series is one whose statistical properties do not depend on the time at which the series is observed. 1

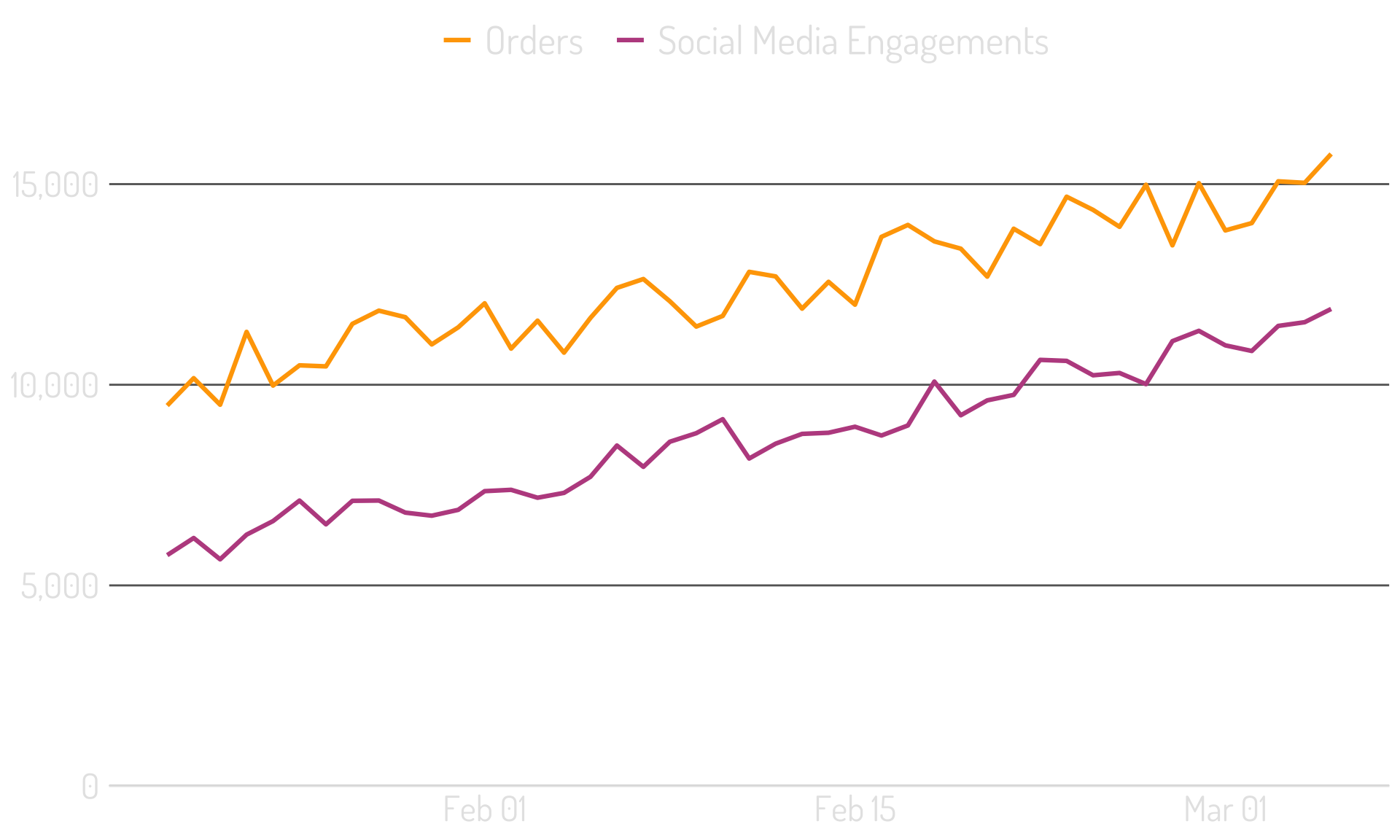

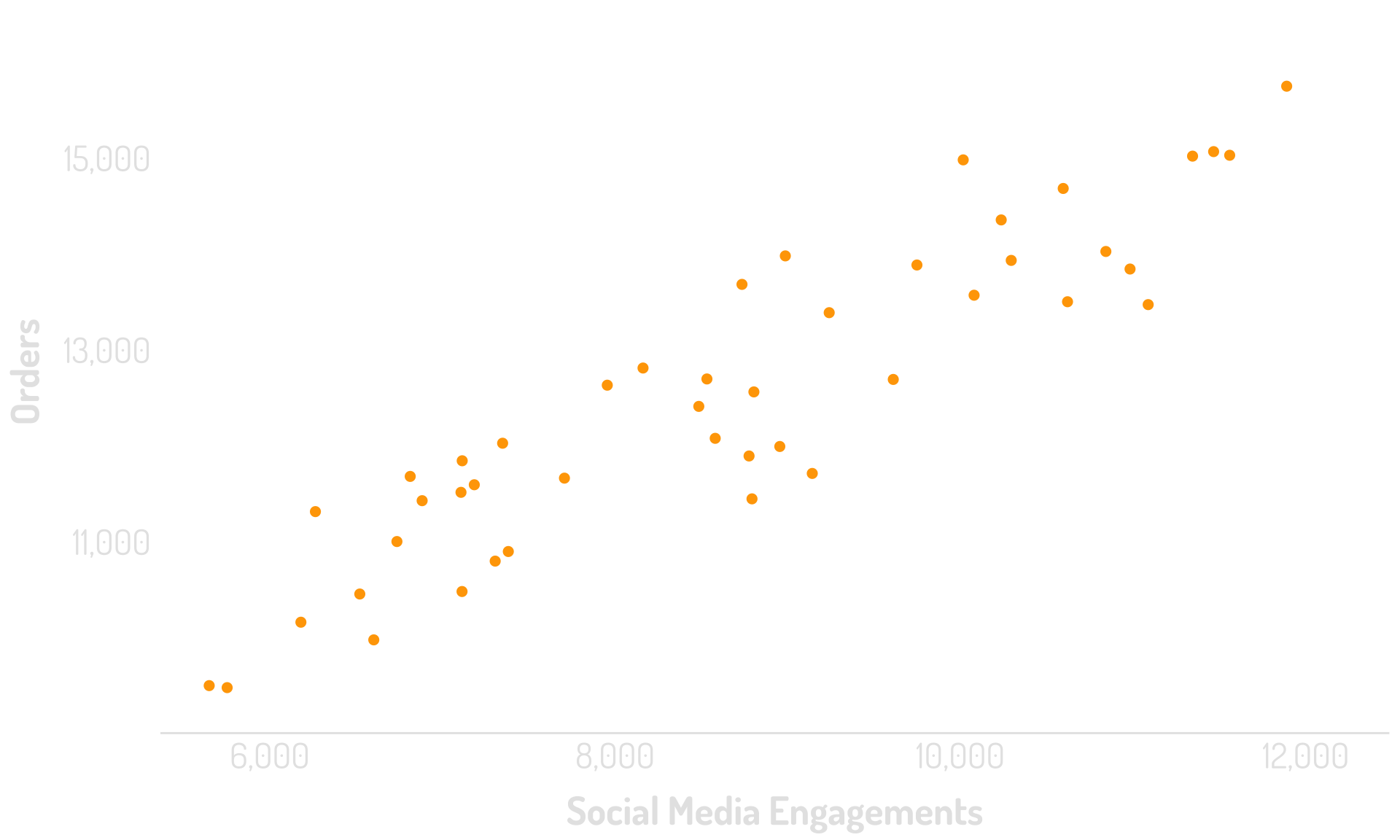

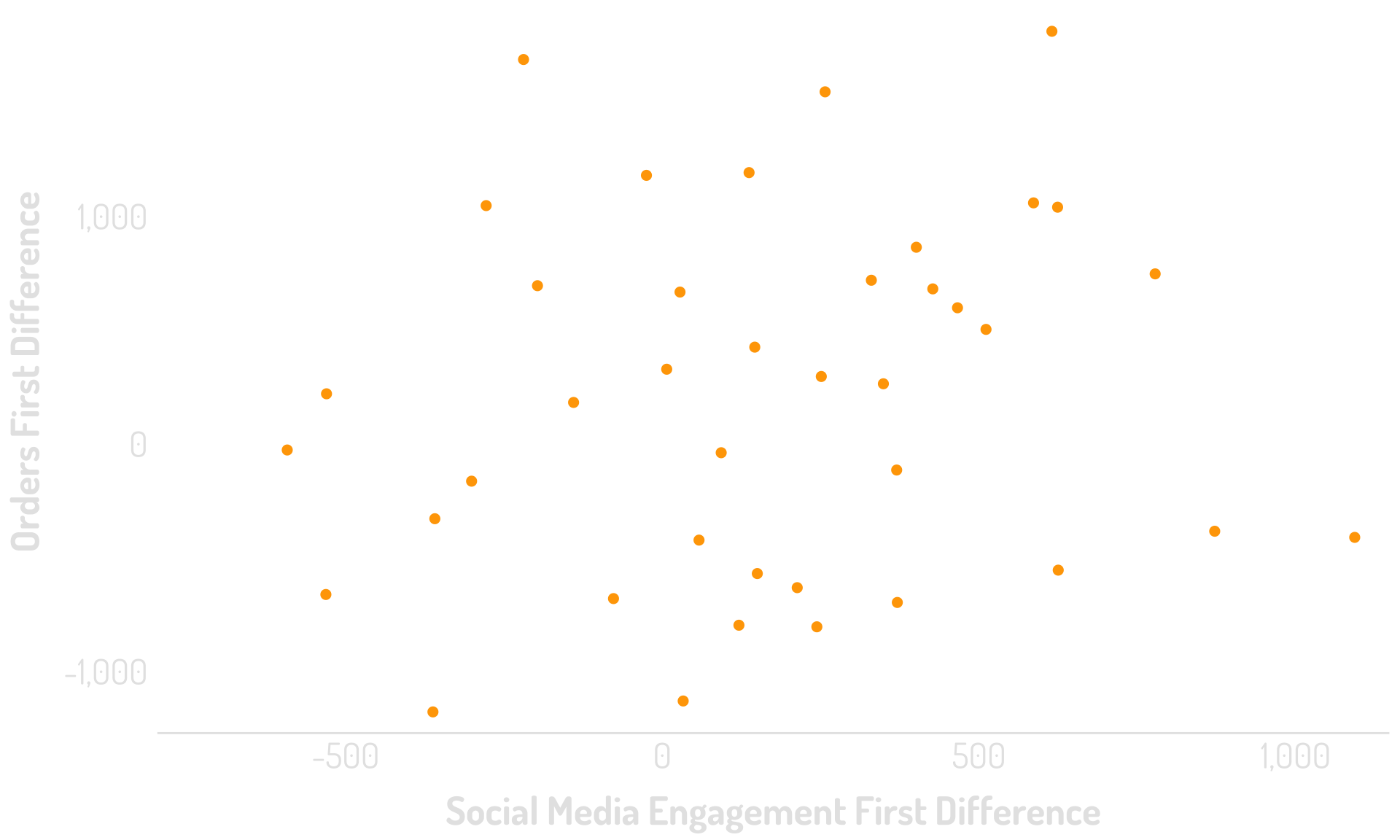

Are these two metrics correlated?

To the scatterplot!

R2 = 0.84

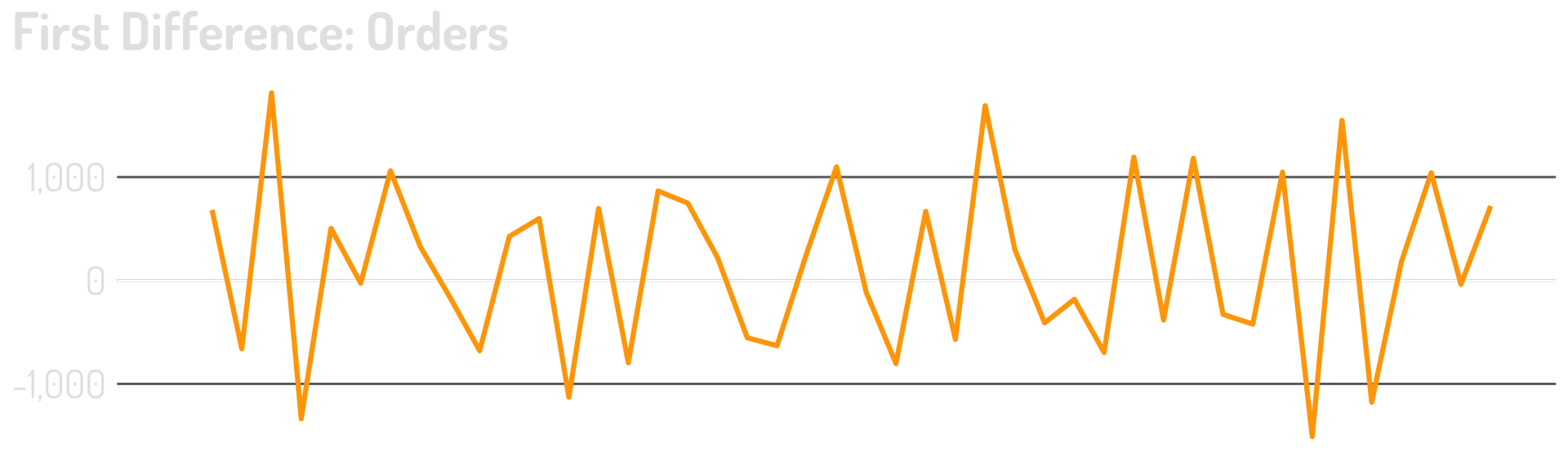

From non-stationary to more stationary

And then check the correlation!

R2 = 0.00

These are both moving with time…but not directly with each other

Let’s shift gears

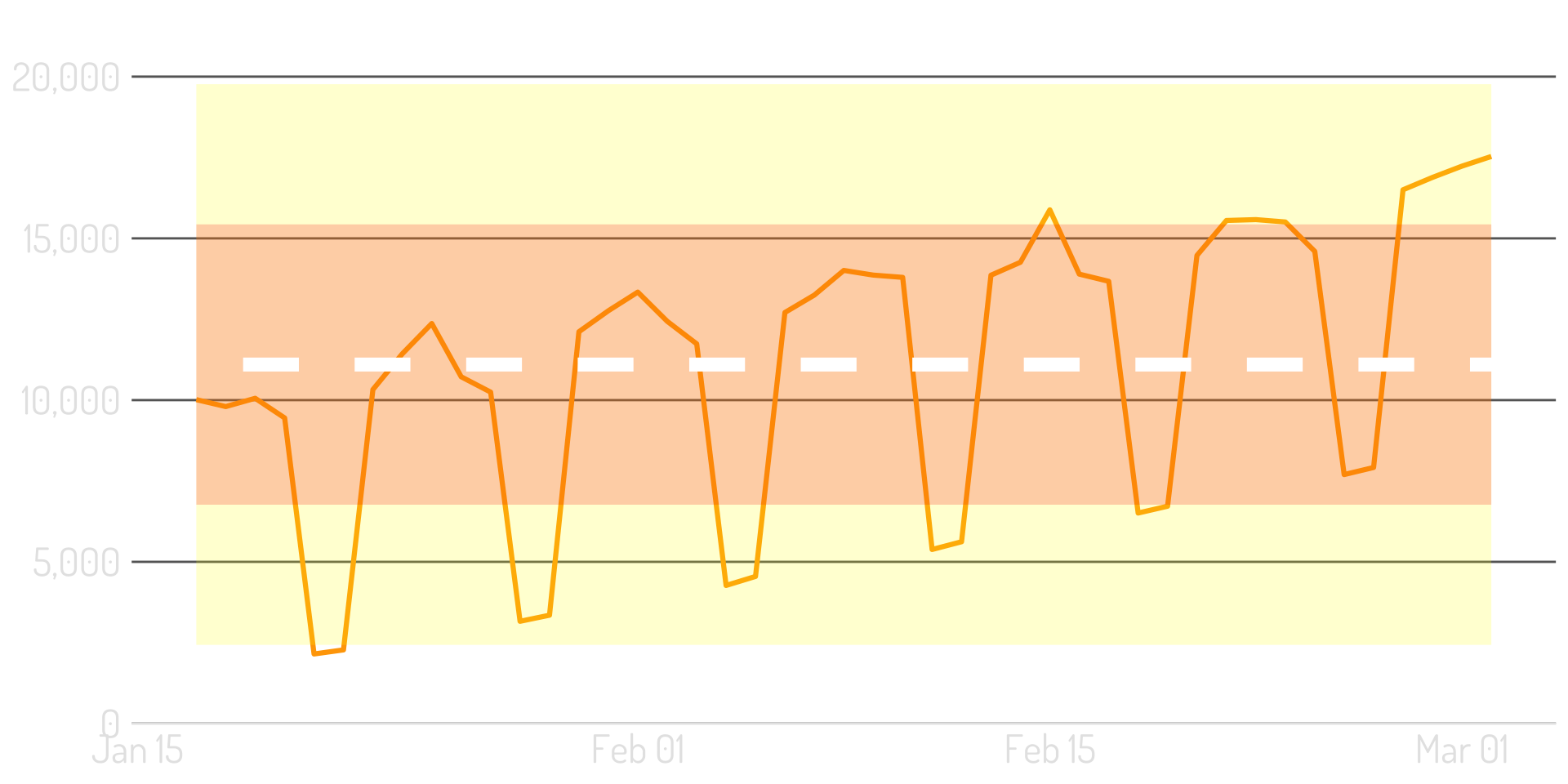

Decomposition can be amazing

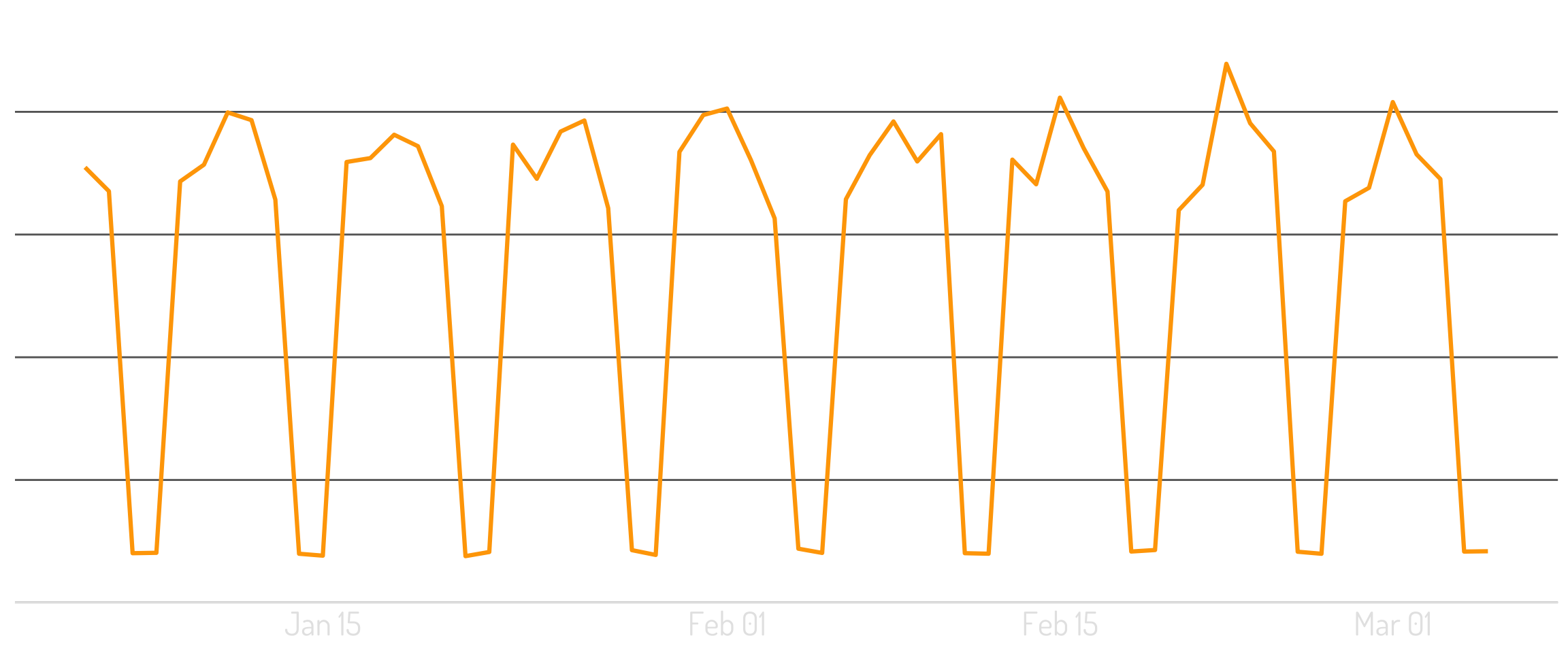

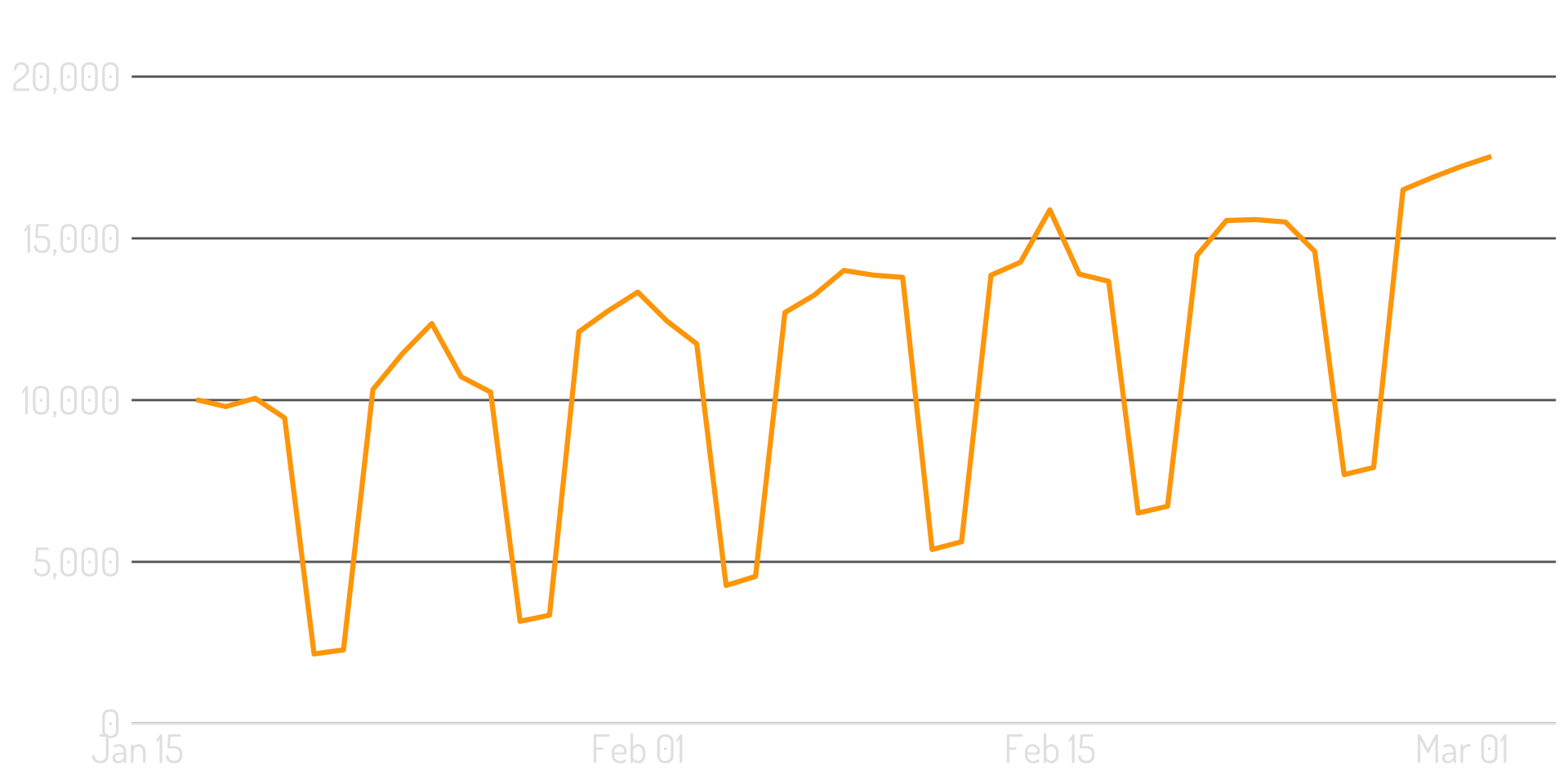

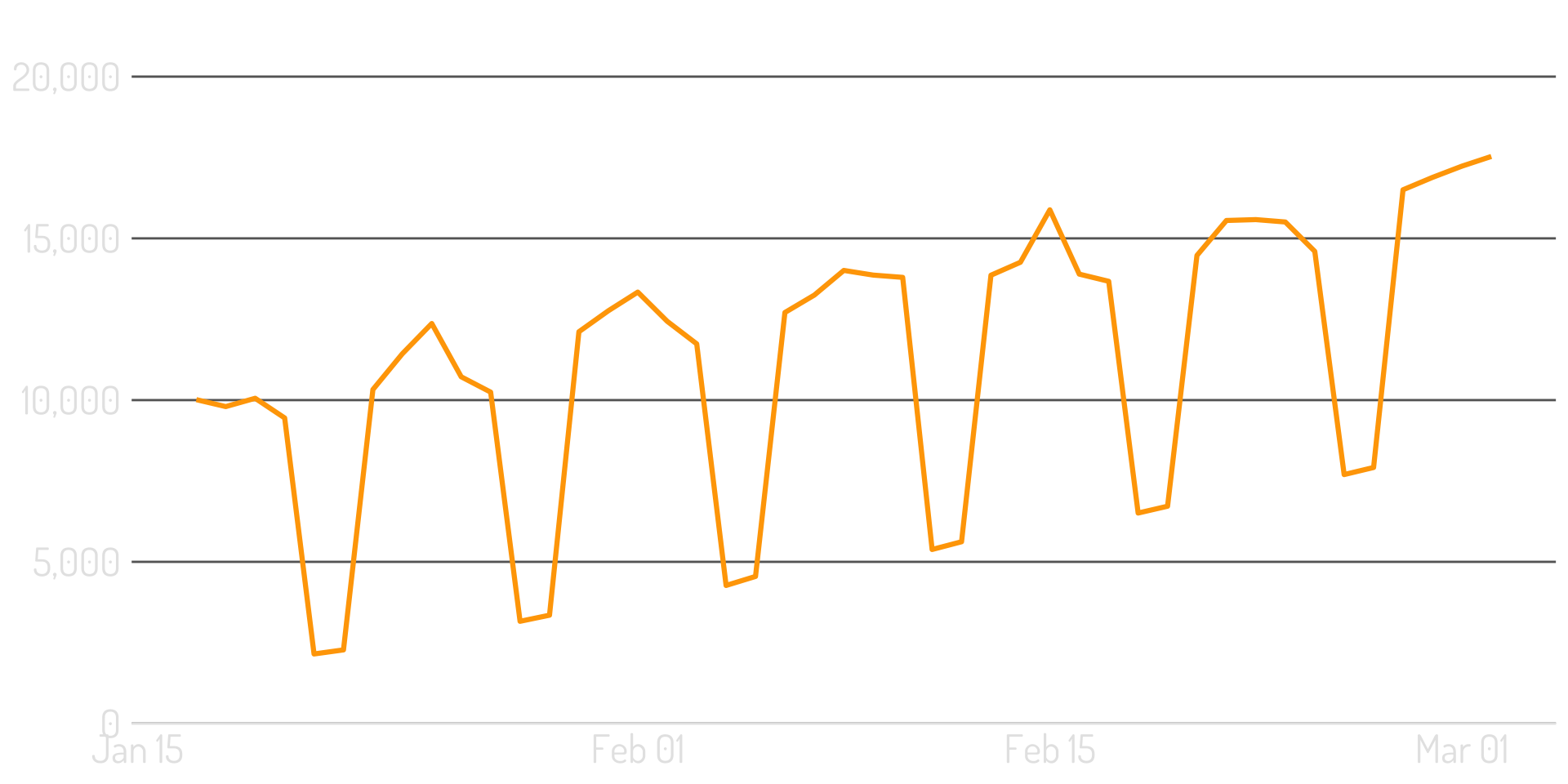

A fairly “clean” series

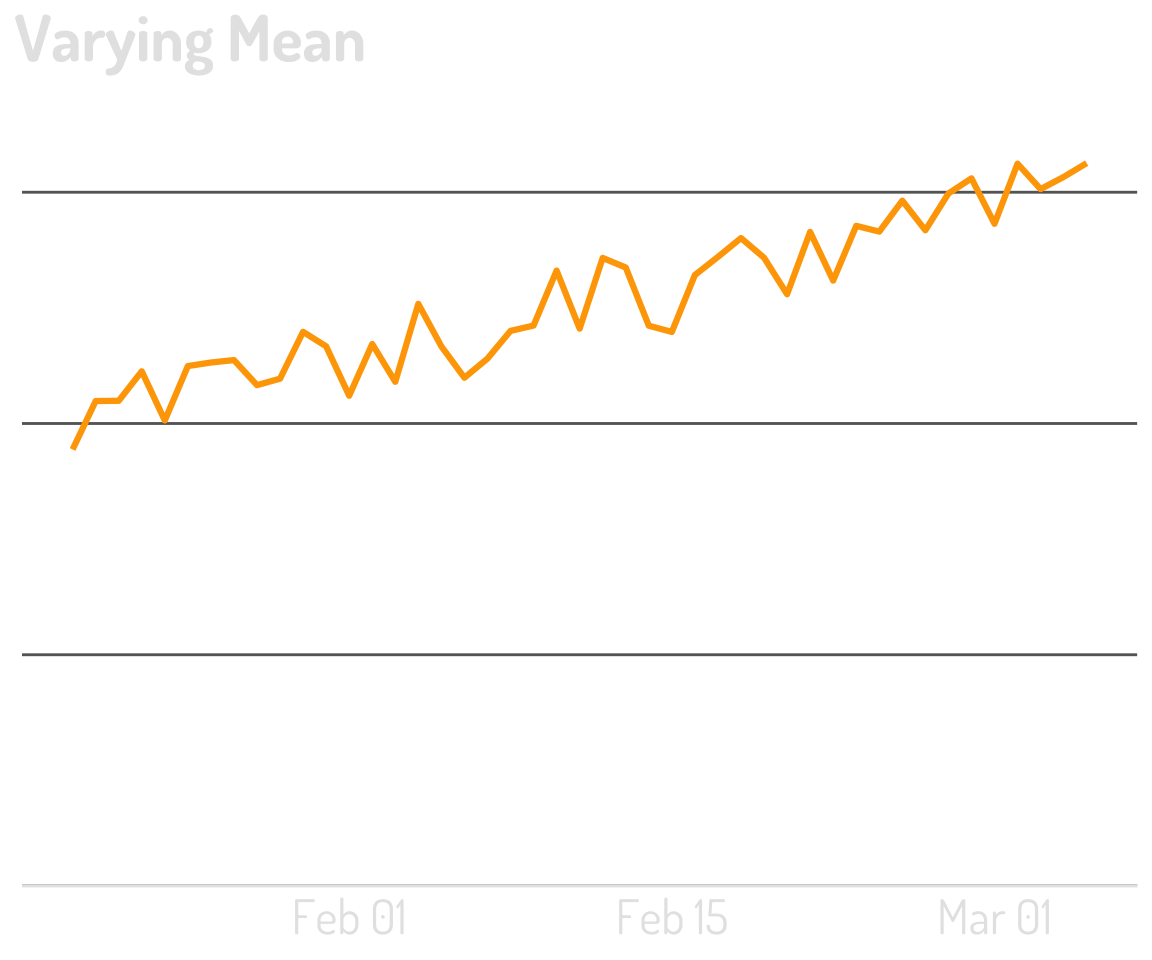

The mean…is pretty meaningless

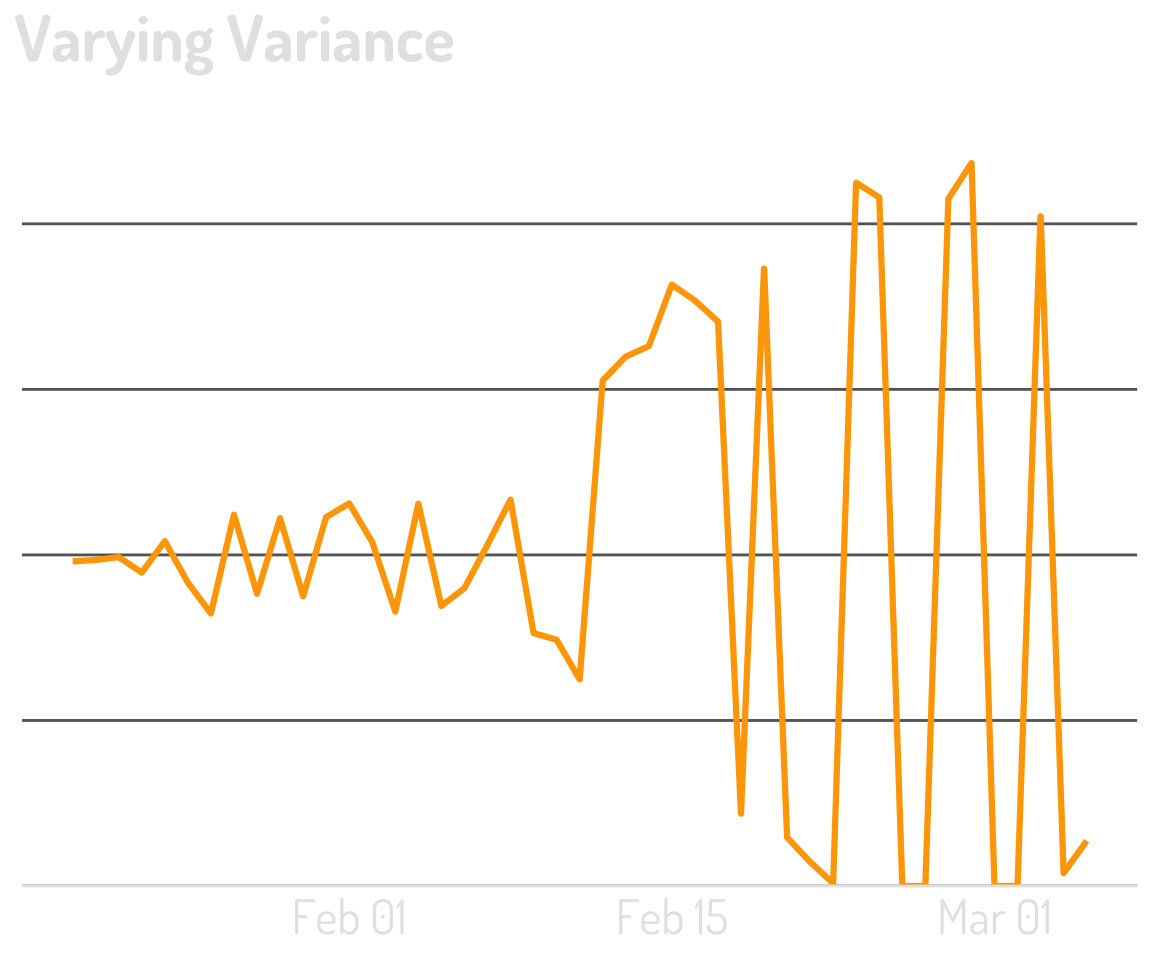

And so is the variance

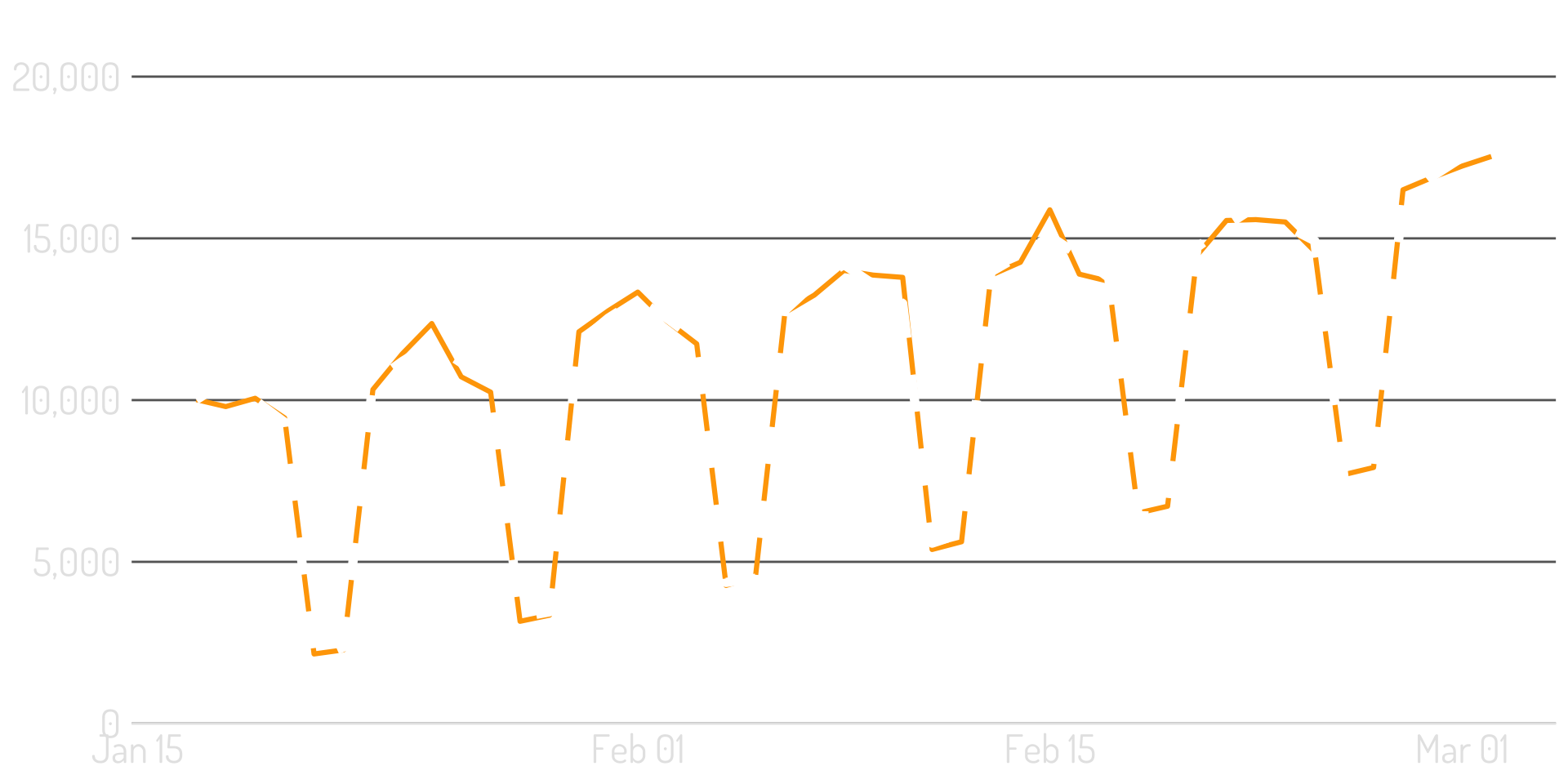

It “decomposes” the data into three components

It “decomposes” the data into three components

The Seasonal Component

The Trend Component

What’s Left!

“The Mean”

“The Variance”

Back to the overall series

The original mean + variance…embarrassing?

Let’s try again

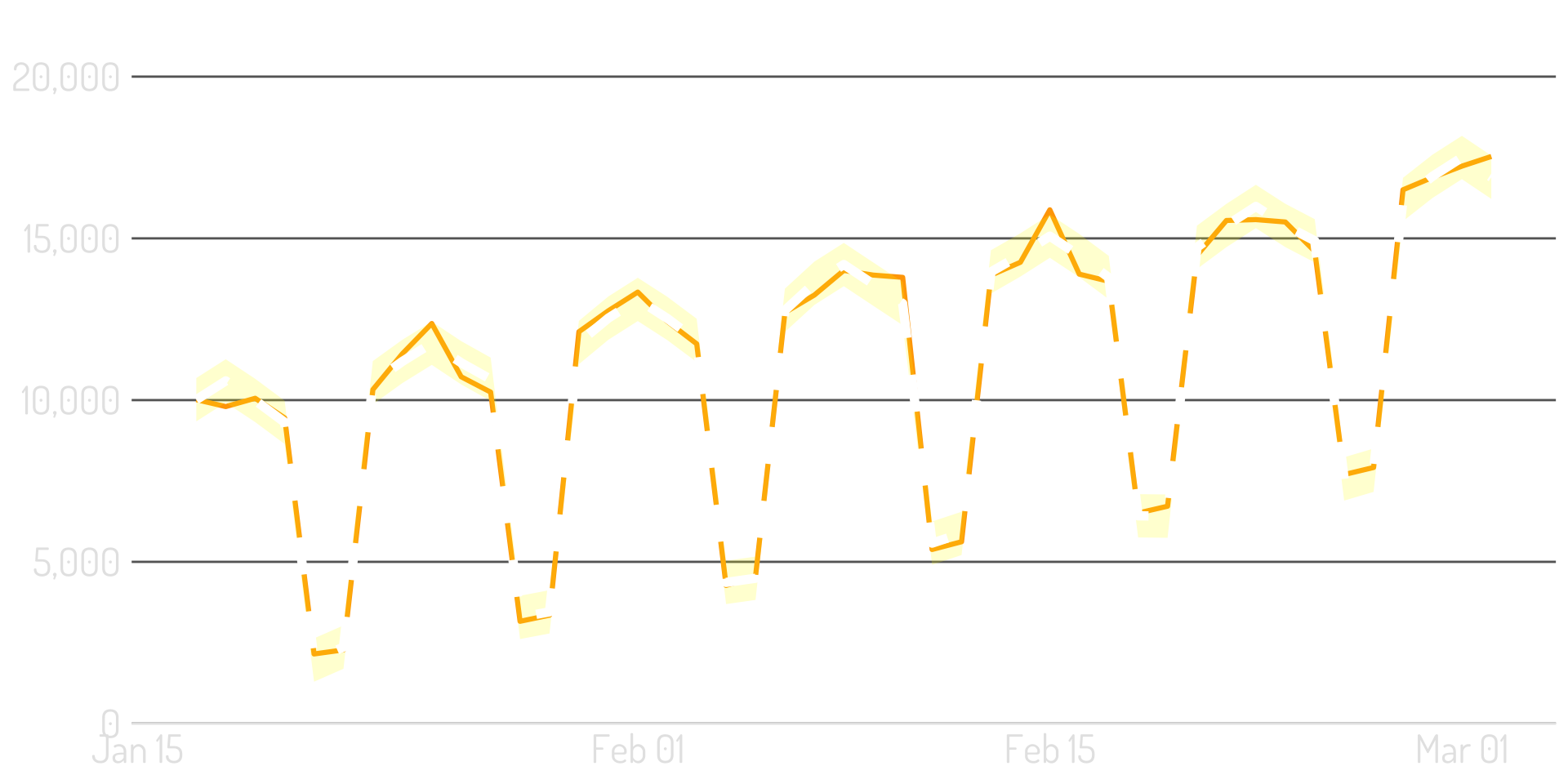

Seasonality + trend = the “mean”

And the “variance” is just based on “what’s left”

This is powerful!

And now…to Bayesian things!

Specifically, Bayesian Structural Time-Series

Time-series decomposition turned up to 11

Mark Edmondson built a tool using this 7 years ago!

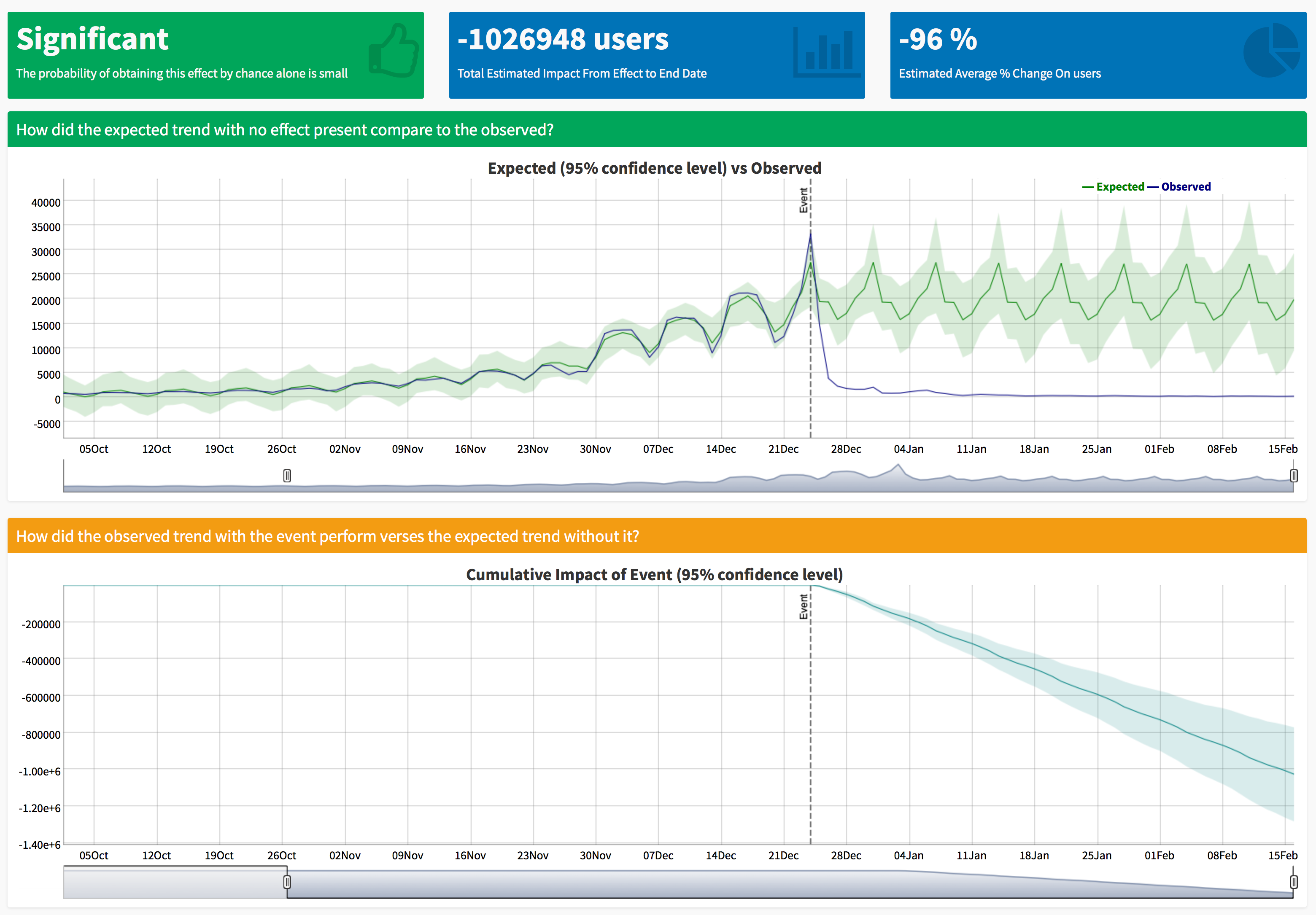

At its core: estimate the impact of an intervention

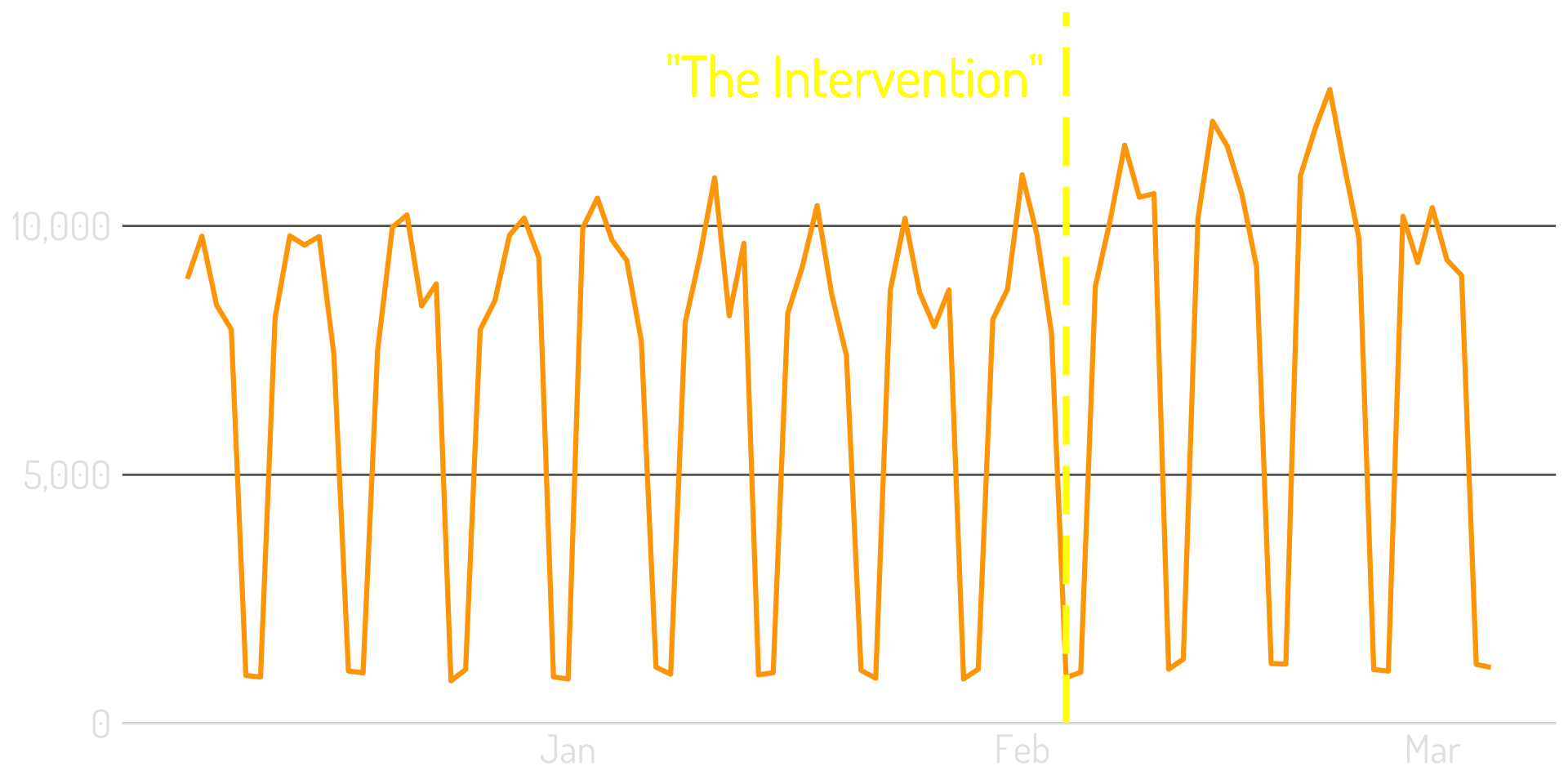

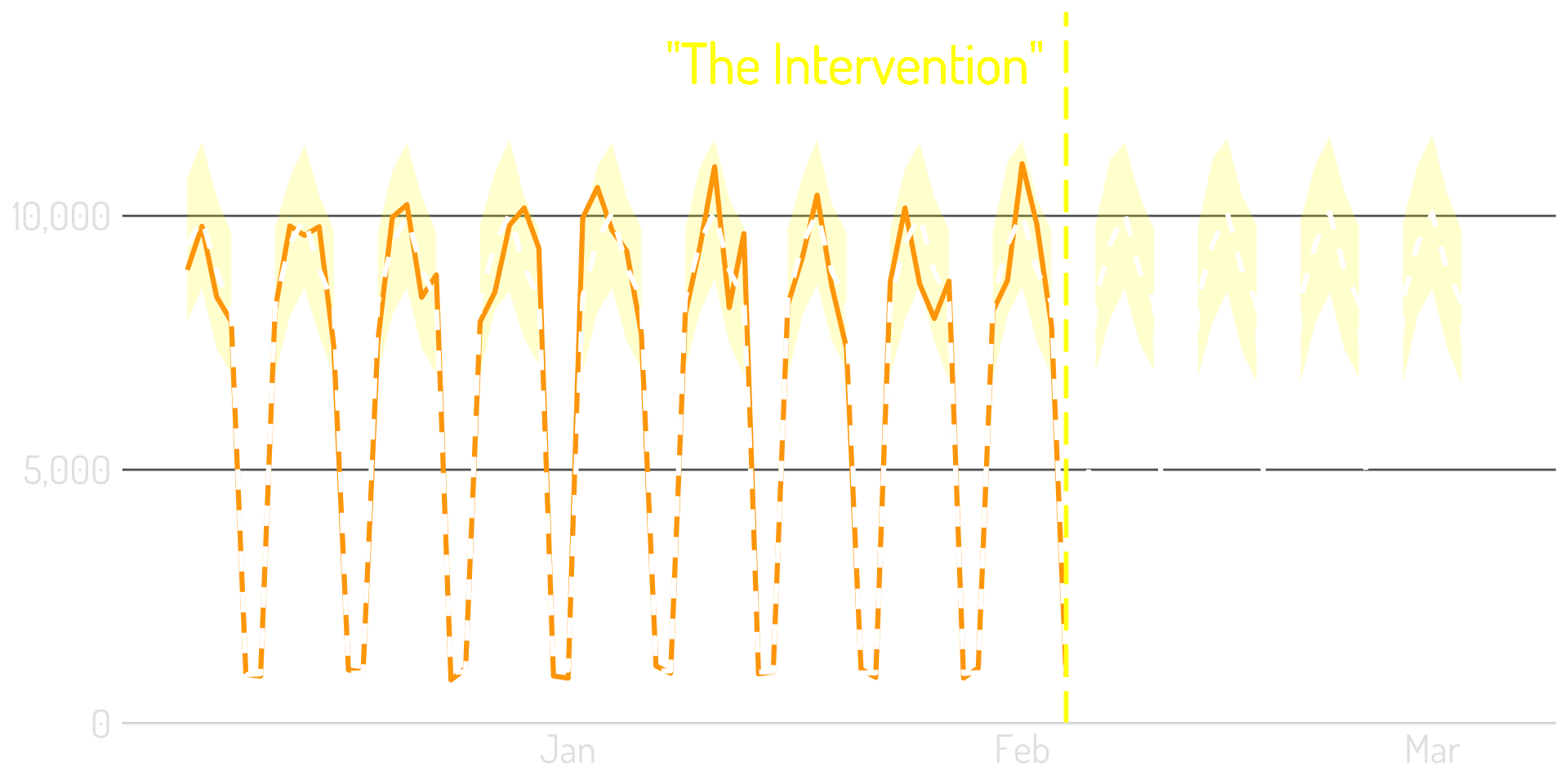

“We didn’t test it, so can we just do a pre-/post- analysis?”

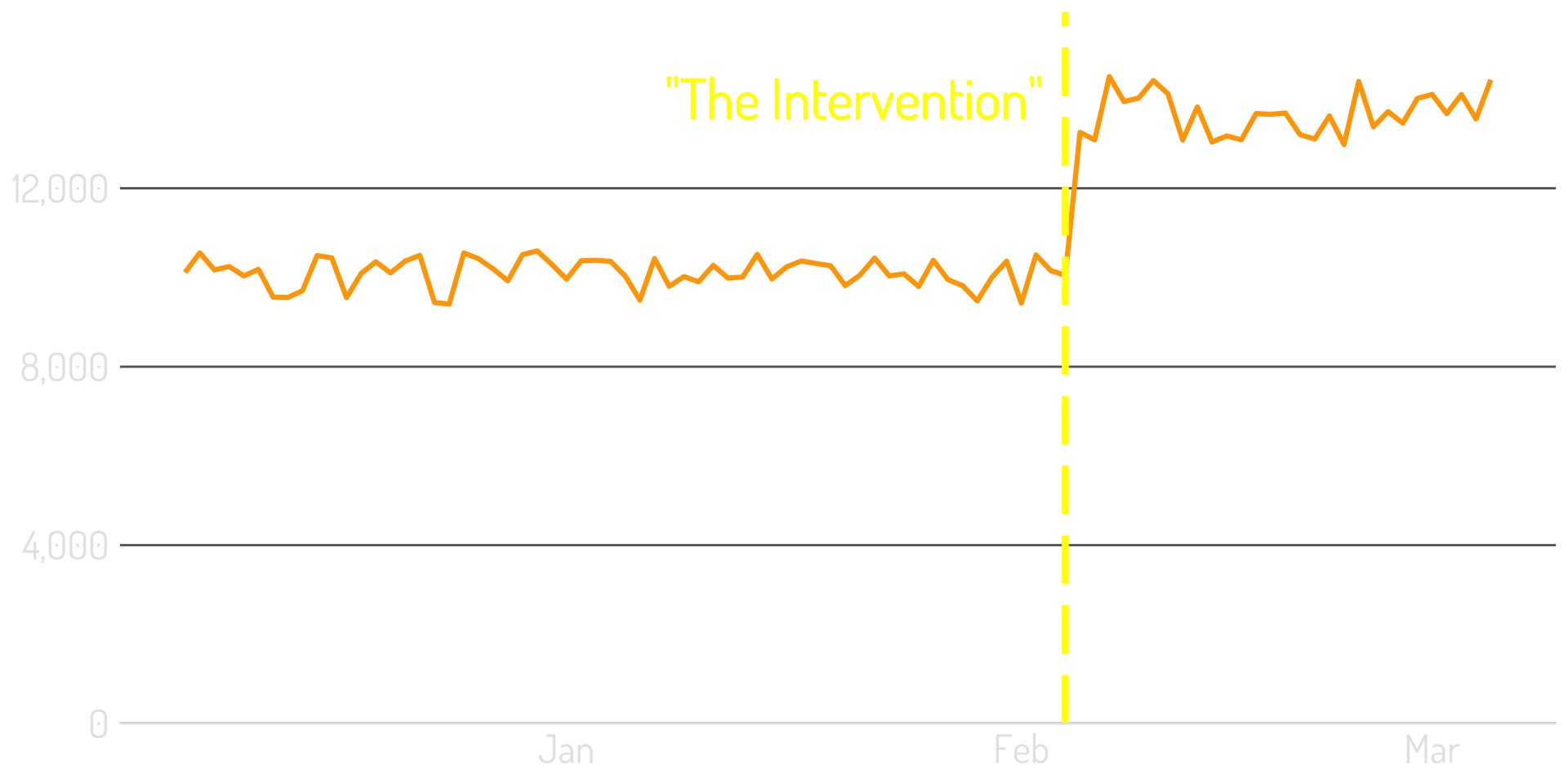

What the marketer expects happened

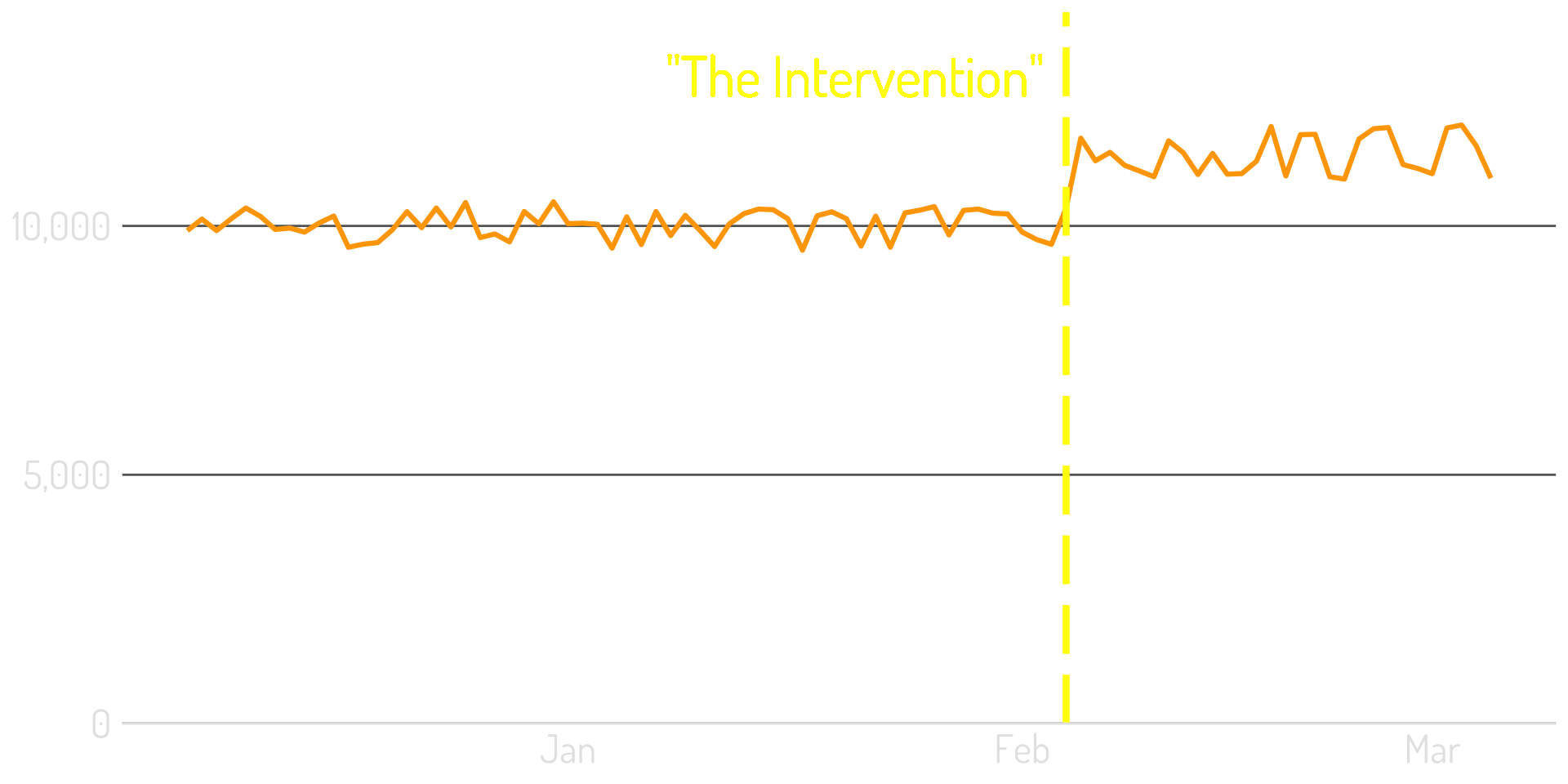

Typically, the change isn’t that big…

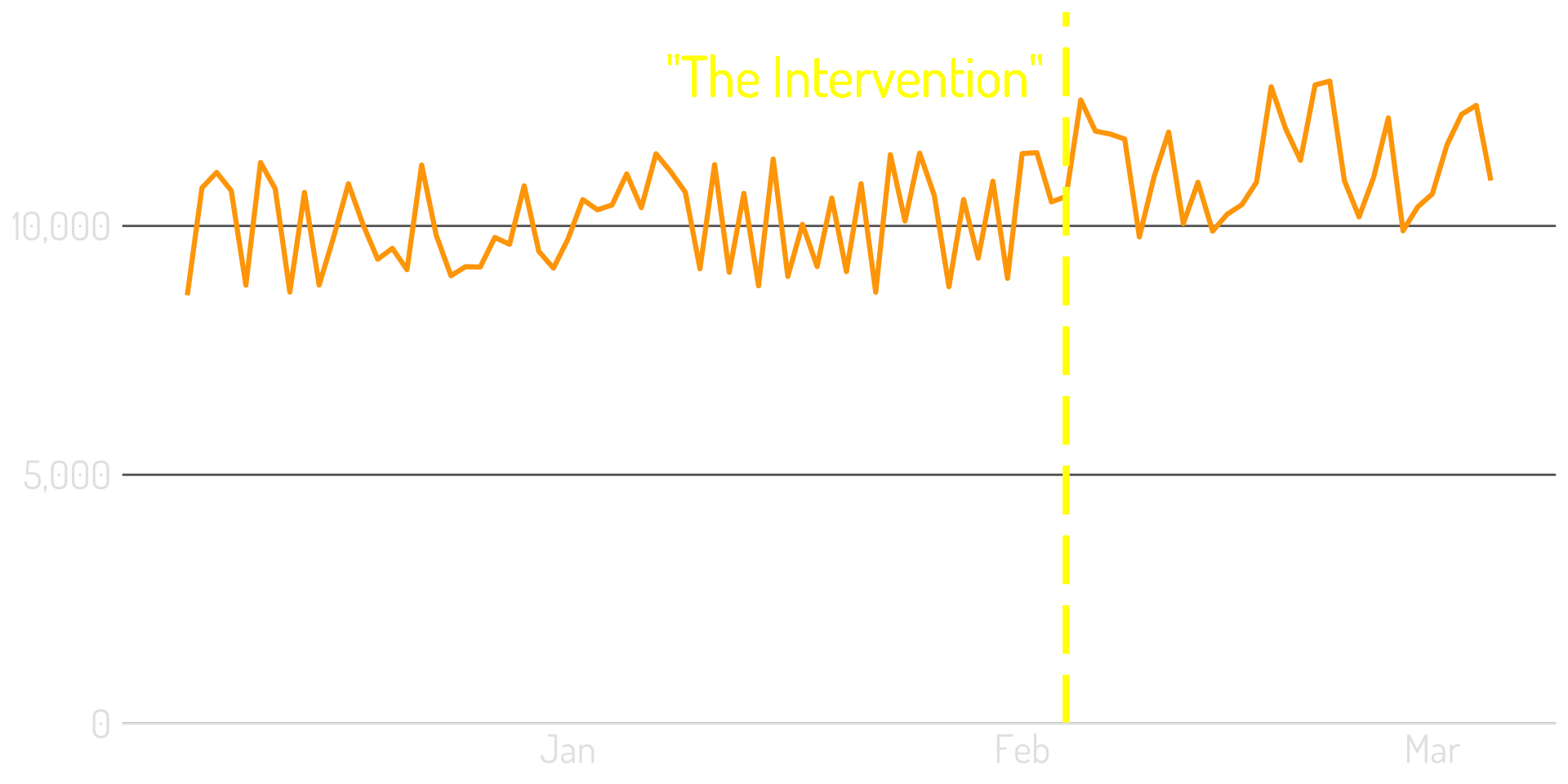

…and the data is a lot noisier…

…and may have seasonality!

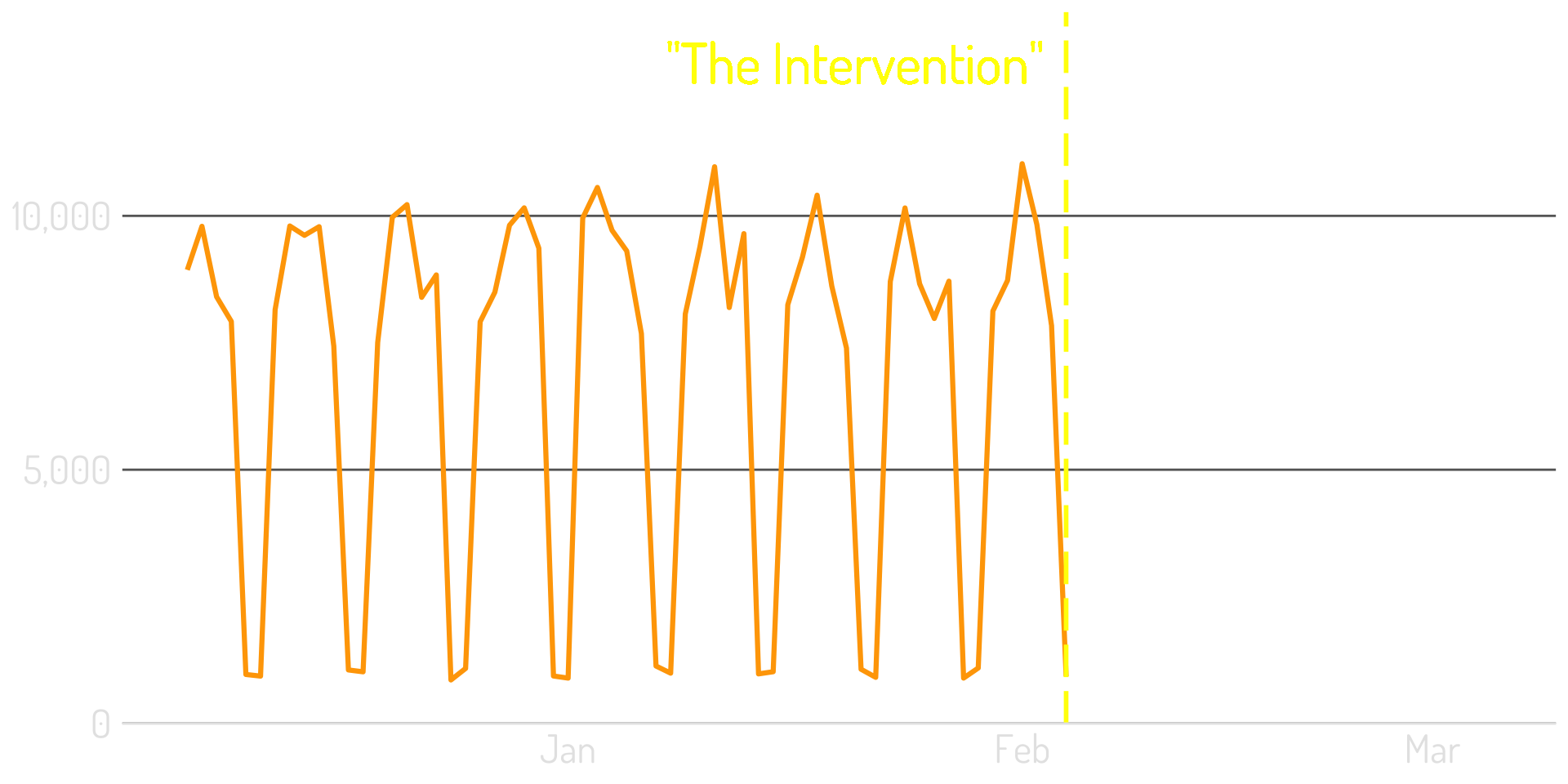

Step 1: Look at the pre-intervention data

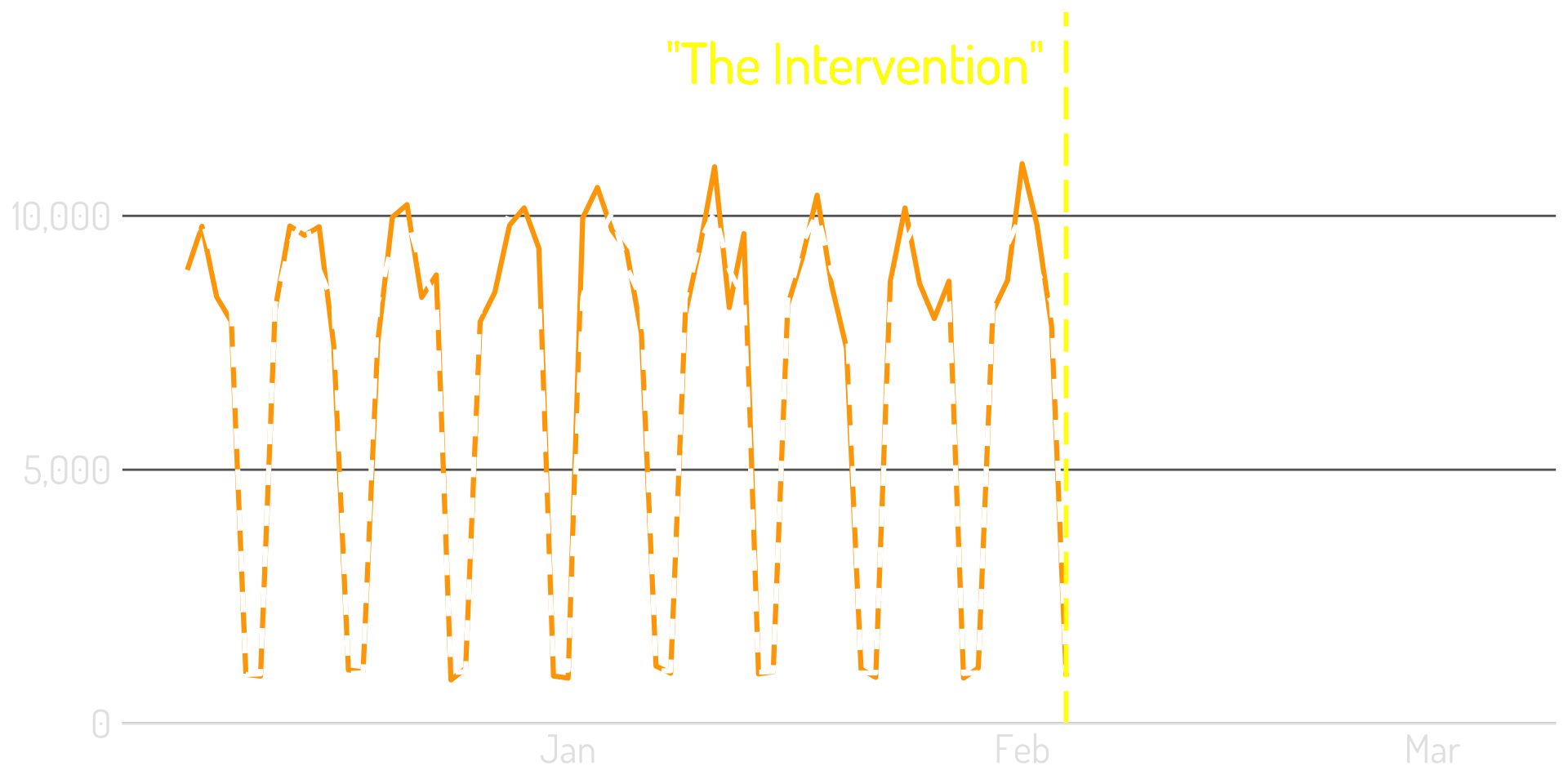

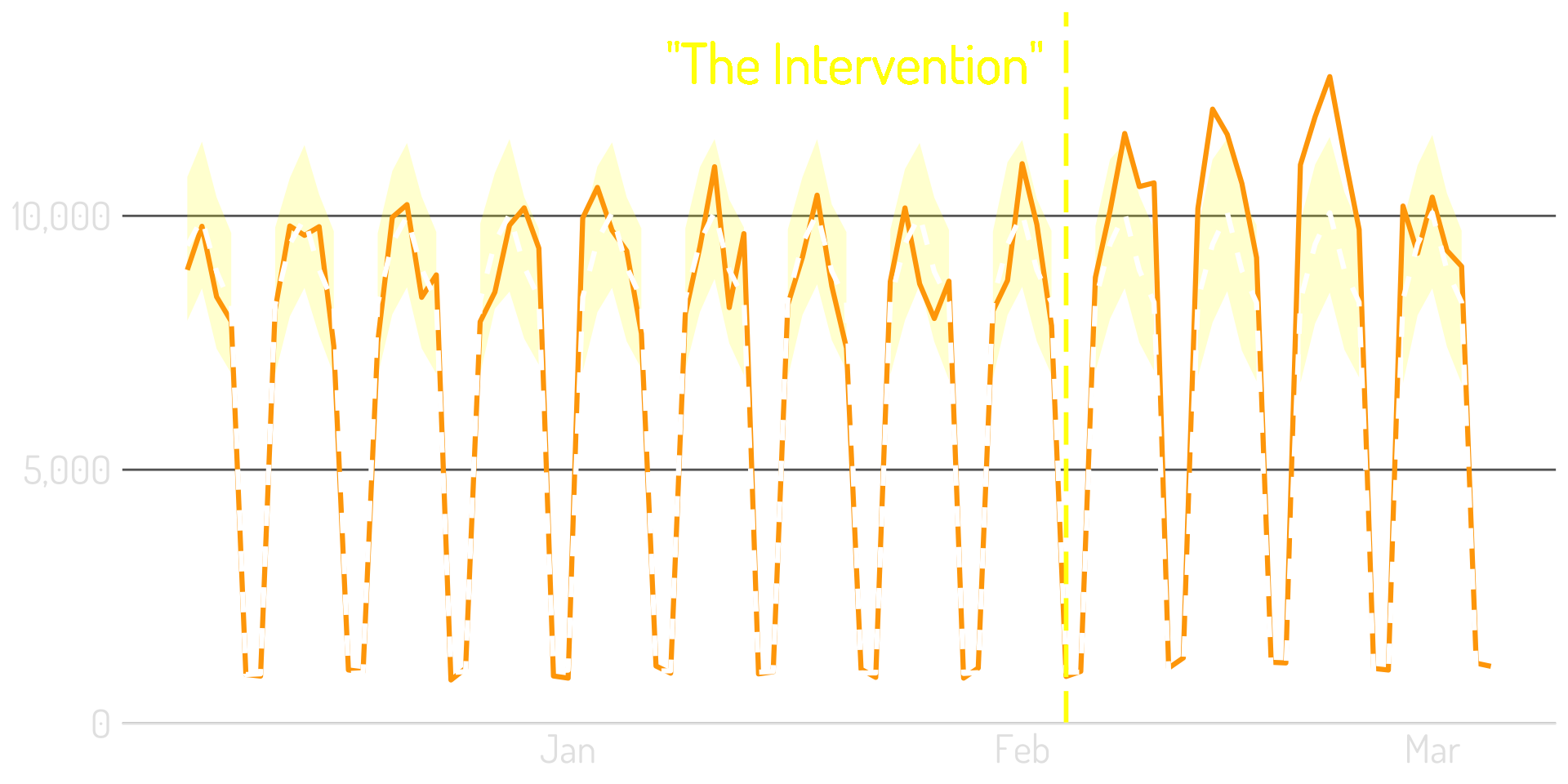

Step 2: Build a best-fit model using this data

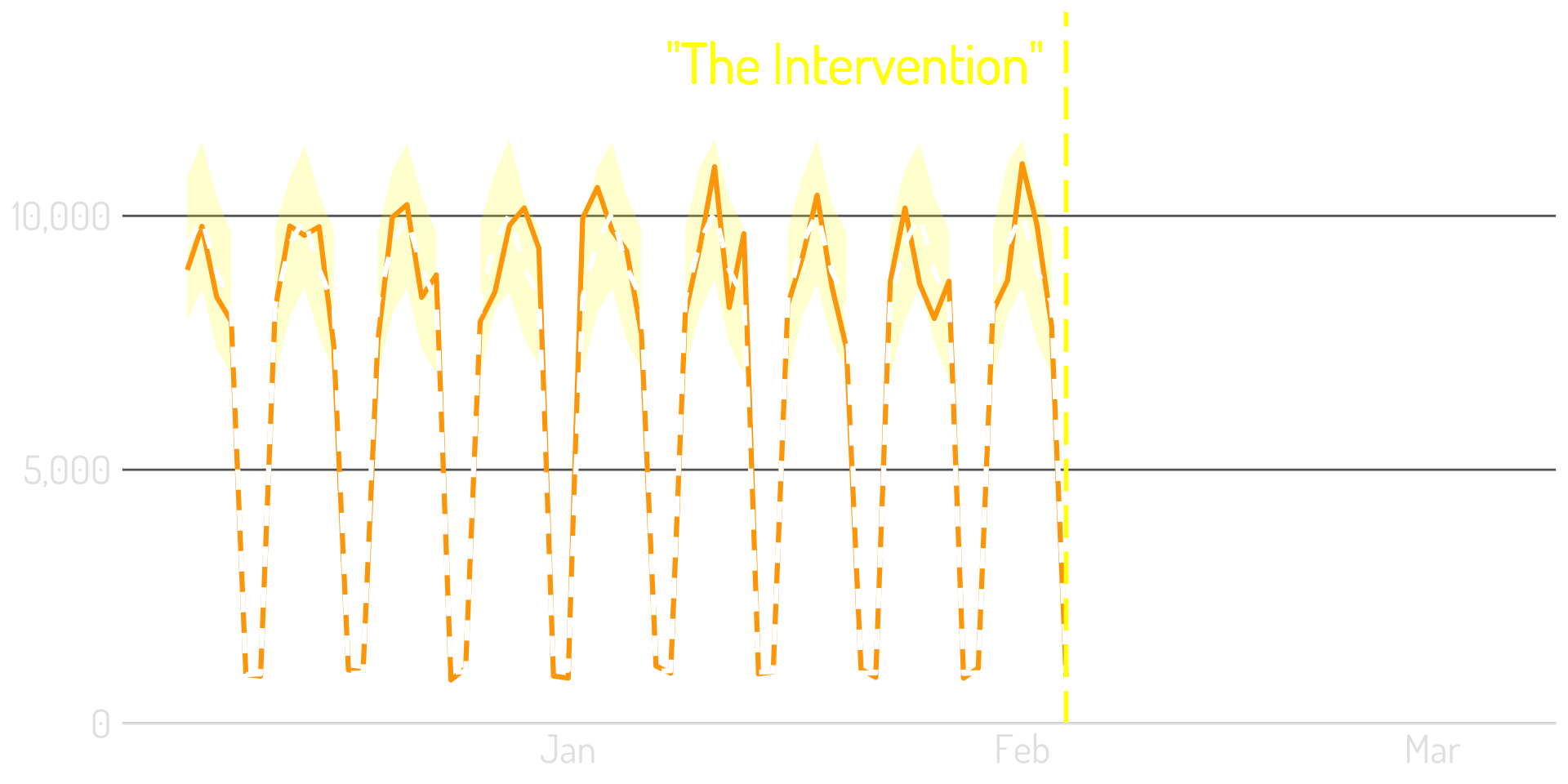

Step 3: That model can quantify its uncertainty

Step 4: Extend the model post-intervention

Step 5: Compare the model to the actual results

Set the modeled prediction as the baseline

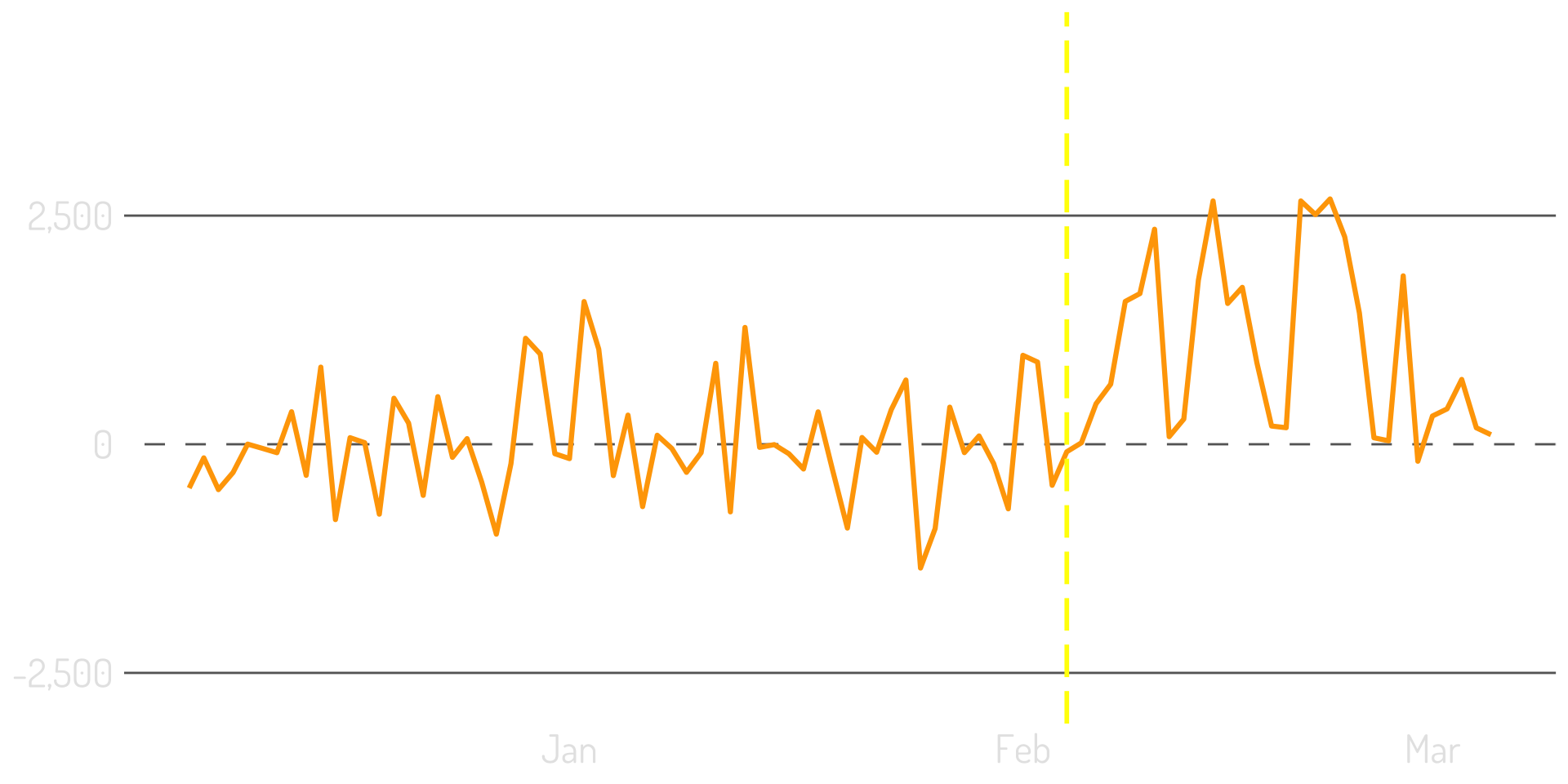

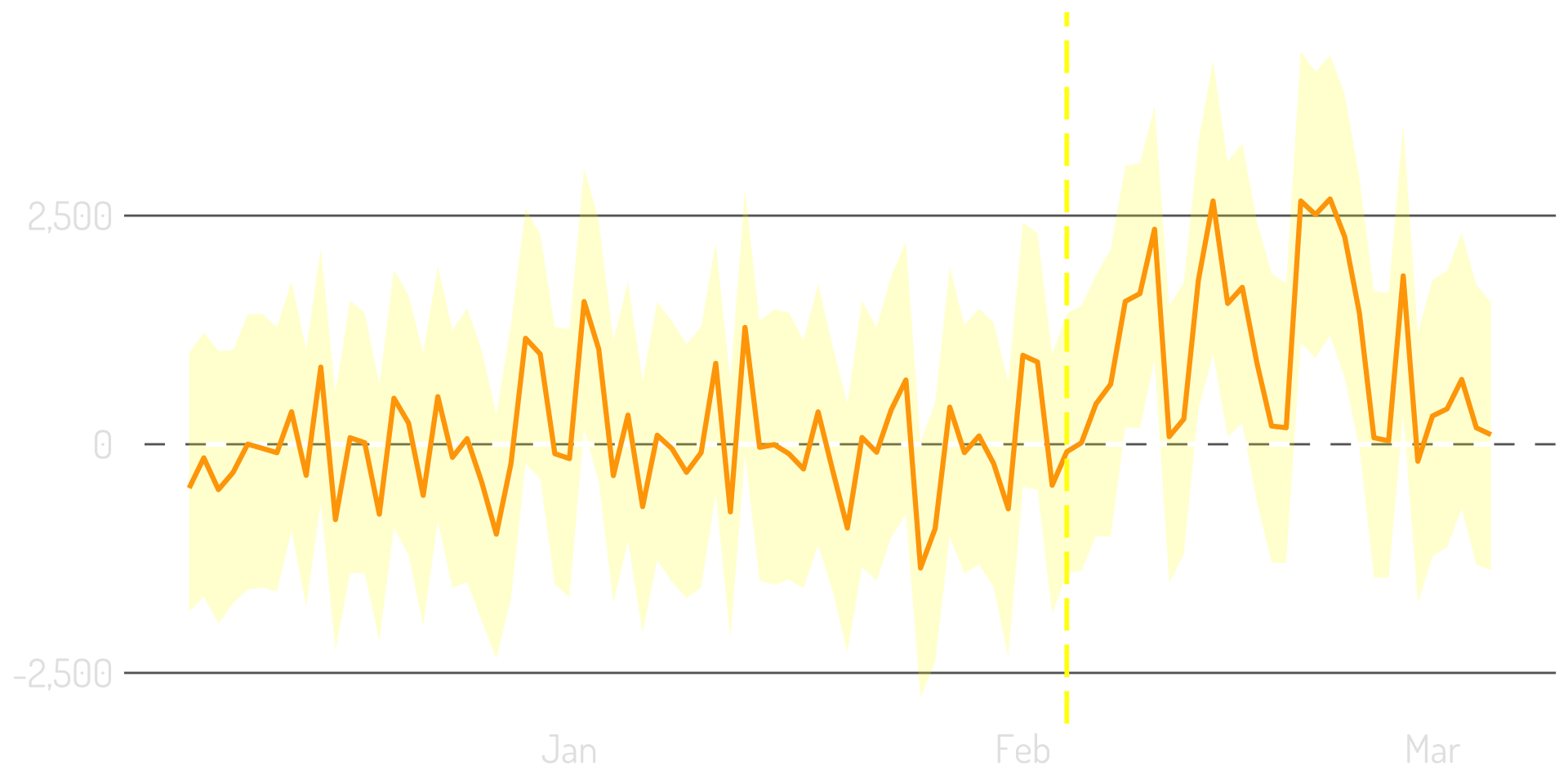

Plot the difference between the model & the actual

Put the confidence interval around the difference

Their relationship to the metric of interest is stable

They are not themselves affected by the intervention

This is not a silver bullet!

What is “the population?”

Regardless…“the sample” is not ideal

Stationarity: constant mean, constant variance

First differences: don’t jump to correlations

Time-series decomposition

Bayesian structural time-series

Time…is hard.

Thank you!

Presentation: bit.ly/sw-time-series

Podcast: analyticshour.io

LinkedIn:

![]() This presentation was 100% built with R (and Quarto w/ reveal.js)

This presentation was 100% built with R (and Quarto w/ reveal.js)

![]() The images are (almost) 100% DALL-E 2

The images are (almost) 100% DALL-E 2

![]() The background image is from my “daily diversion” on Twitter

The background image is from my “daily diversion” on Twitter